Borrowing money

We understand that the cost of living crisis is troubling for many but we are here to offer you monetary guidance and support. There are support measures in place from the government to help you and remember, if you work in racing, you are never alone; our welfare officers and advisors are here to help over the phone on 0800 6300 443.

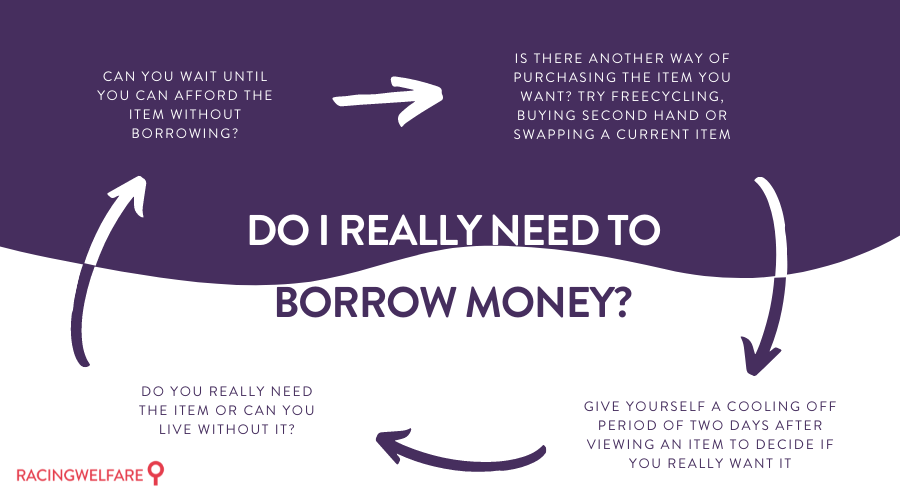

Do you really need to borrow money?

Before you sign up for a credit card, bank loan or store card, or add to an existing card or loan it makes sense to think about whether you really need to borrow money.

There are some very important questions you need to answer before you borrow money. You should ask yourself if you need to spend the money, if you have other ways of financing the purchase and if you can afford to pay back the money you’re planning to borrow.

Can you save up or use some savings instead of borrowing money?

If you really don’t need to spend the money today, then you should seriously consider saving some money each month rather than getting into debt.

If you can wait and save up for a purchase, instead of using credit, it will cost you far less (unless you qualify for a 0% credit card deal), as you won’t have to pay any interest. It might also have been reduced in a sale or if it’s technology, upgraded to a better model.

Example

If you wanted to buy something that cost £600, the following options should be considered:

1. Saving before you spend

If you don’t have any savings, but can save, for example, £50 a month, it would take you a year to save the £600 and you would have earned £6 in interest (assuming you’re a basic rate taxpayer – which means 20% tax comes off the interest you earn – and that you put the money into an account paying 3% in interest).

2. Cashing in savings

If you used the money from your savings account; assuming your savings earned 3% a year and that you paid tax at the basic rate (of 20%), you would lose a maximum of £14.40 in interest if it took you a year to save the £600 again. That means spending £600 from your savings would ‘cost’ you a maximum of £614.40 by the time you’ve added in the lost interest.

3. Using a credit card

If you paid the £600 by credit card, charging an average interest rate of 17%, and if you paid the debt back at a rate of £50 a month, it would take you 14 months to repay the debt and would cost you £58 in interest. That means you’d be £43.90 (£58-£14.10) worse off by paying on your credit card, rather than cashing in your savings.

Good money borrowing versus bad money borrowing

Example 1 – Sarah is a teacher who travels to work by bus each day. She gets a better job at a new school paying a higher salary, but she can’t travel there on public transport. She wants to buy a car but doesn’t have enough savings to cover the cost so she needs to borrow some money.

This is good borrowing as Sarah’s job is paying her more money. She will recoup more than the cost of the car, including the money she borrowed. Of course, it depends on the kind of loan she gets and how much it costs relative to her increased pay.

Example 2 – Andrew wants to trade in his old car for a new one. He thinks he’ll need to spend £5,000 to get a reasonable car. He doesn’t use his car for work but likes the freedom that having a car gives him.

He can get £500 for his old car and he can afford to pay back £100 a month if he borrows the rest. It will take him five years to repay the loan and he’ll have paid a total of £5,923, or £6,423 for the car including the trade-in.

Andrew should think very carefully about taking out this loan as he will end up paying an extra £1,423 for his car and will have to make loan repayments for the next five years. If his situation were to change in that time (say, his hours were reduced or he lost his job), he might not be able to keep up the repayments.

Money Advice Service – Good debt versus bad debt

If you do decide you want to borrow money

If you definitely want to borrow some money and you are sure you can repay it, there are a number of important factors to consider.

How much can you afford to repay?

Top Tip

Almost two thirds of people clear their credit card bills in full every month. Even if you can’t pay it all off, make sure you don’t just make the minimum repayments on your credit card bill.

It’s very important to work out how much you can afford to repay each month, as this will affect which borrowing option is best for you.

Make sure you are realistic about how much you could pay if your mortgage or rent went up, if you had to spend more on things like energy bills or if your pay was cut.

Money Advice Service – Working out a repayment plan for money you are borrowing

Choosing the right type of credit

You should also make sure you choose the right type of credit or loan for your situation. Otherwise you could find yourself paying more than you need to. Shop around and compare deals, looking at:

- The interest rate and the APR

- The cost per week or month and whether this may vary

- How much you will repay in total, and

- Any penalties for missed or late payments

Not all credit options are good or safe. If you have a poor credit rating then you may be tempted to use a doorstep lender or a payday loan company, especially if you have few credit options. However, these are expensive and should be avoided for anything more than a few days if possible.

Money Advice Service – Deciding on the best type of credit for you

If you work in horseracing and you need financial support or advice, we can provide you with 24 hour support and give you the guidance you need.

Get Support Now

Racing Welfare’s 24 hour support line enables people to access support and

guidance through digital and telephone options.

Related Articles

Free gambling awareness workshops

Statutory Sick Pay

Which bills to pay first?

Understanding your payslip